It is not a stretch to claim that economic volatility seems to be the new normal, leading high-net-worth (HNW) individuals and their advisors to increasingly seek solutions which go beyond traditional investment models. At Cedar Point Financial Service LLC, we recognize that as tariff and inflation uncertainty surges, markets oscillate, and tax laws remain in flux, the need for financial strategies that can both withstand disruption and create durable value has never been greater.

A recent white paper from Ernst & Young (EY) adds quantitative rigor to a message that sophisticated advisors have intuitively understood: integrating permanent life insurance into a comprehensive financial plan provides both resilience and outperformance compared to investment-only approaches. The research shows that a portfolio incorporating permanent life insurance and, to a lesser extent, deferred income annuities (DIAs), delivers improved risk-adjusted retirement income and significantly greater legacy outcomes.

While annuities play a complementary role, the primary takeaway for HNW clients is this: permanent life insurance is not just protection against mortality risk - it is a core asset class with unique planning benefits that can be mathematically quantified and optimized.

From Death Benefit to Asset Class: Redefining the Role of Life Insurance

Traditionally, life insurance has been viewed narrowly: a tool for estate liquidity, often invoked to pay estate taxes or replace income. But this limited view underestimates the strategic versatility of permanent life insurance. Increasingly, life insurance is being redefined as a contingent asset class - an investment with low correlation to financial markets, minimal standard deviation, and a risk-adjusted return profile that enhances overall portfolio efficiency.

According to a Trusts & Estates article by Jay C. Judas and Michael Fontanini, properly structured life insurance policies - especially participating whole life and various types of universal life (fixed, indexed, variable and private placement) - can be modeled within the framework of Modern Portfolio Theory. They demonstrate that life insurance provides a predictable return with an exceptionally low standard deviation (0.47% in one case study in the article), making it a valuable addition to any diversified wealth transfer portfolio.

The EY Research: Stress-Tested Performance in a Volatile World

In the EY white paper, researchers simulated 1,000 economic scenarios using Monte Carlo modeling, evaluating outcomes for various asset allocations across three metrics: after-tax retirement income (with a 90% probability of success), wealth at retirement, and legacy value at death. The integrated strategies that included permanent life insurance consistently outperformed investment-only or term-life-plus-investment strategies.

Key findings:

- A portfolio with just 30% allocation to permanent life insurance generated 2.0% more income and 13.4% more legacy value than investments alone.

- Permanent life insurance performed better than term insurance, which provided less income and smaller legacy values due to its lack of cash value and compounding growth.

- In periods of market volatility, policy surrenders and/or loans from permanent life insurance served as a tax-efficient income bridge, allowing the portfolio to recover rather than being forced into premature liquidation.

These results underscore that permanent life insurance is not a drag on portfolio performance, as some skeptics argue, but rather a contributor to greater efficiency and long-term stability.

Life Insurance as a Volatility Buffer and Tax Shelter

One of the most overlooked advantages of permanent life insurance is its role as a volatility buffer. During periods of market stress, accessing the cash value of a life policy through surrenders and/or policy loans prevents the need to sell other investments at a loss. This sequencing-of-returns advantage protects the long-term viability of a retirement portfolio.

Additionally, life insurance offers unmatched tax benefits:

- Tax-deferred accumulation of cash value

- Tax-free access to cash via policy surrenders and/or loans

- Income-tax-free death benefit

- Estate tax leverage when owned by an Irrevocable life Insurance Trust (ILIT)

The insurance planning experts at Cedar Point Financial Services LLC work with clients and their advisors in demonstrating how these benefits provide flexibility and stability that are especially valuable when planning across multiple generations or amid tax law uncertainty.

Measuring Risk-Adjusted Return with Sharpe Ratio

EY’s findings align with the contingent asset class analysis featured in Trusts & Estates. Life insurance, when assessed using MPT and Sharpe Ratio calculations, exhibits:

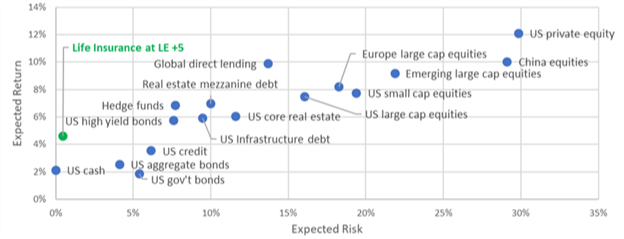

- A risk-adjusted return (Sharpe Ratio) of 9.49, compared to 0.80 for bonds and 0.46 for equities

- A 6.60% equivalent pre-tax return at life expectancy

- Stability across all modeled life expectancy outcomes

Even when assuming a more conservative mortality beyond life expectancy (LE +5 years), the Sharpe Ratio remains compelling at 5.30 - well above other traditional assets. This means that for each unit of risk, life insurance delivers significantly more return, especially in wealth transfer contexts.

© 2020 Lion Street, Inc. Used with permission.

This type of modeling shows why permanent life insurance can be a superior vehicle for the portion of a portfolio intended to support heirs and charitable legacies.

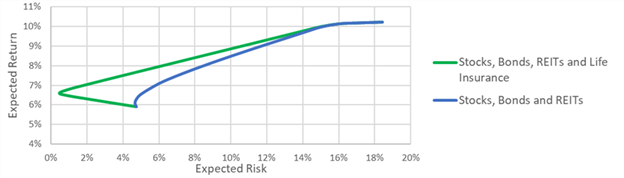

Case Study: Efficient Frontier Implications

The Trusts & Estates article presents a case study of a 60-year-old woman with a $15 million trust. The trustee funds a $10 million universal life policy with premiums of $154,049 annually. At life expectancy (age 89), the policy delivers a 6.6% pre-tax-equivalent return with extremely low risk (standard deviation of just 0.47%). The ROI remains competitive even if the insured lives beyond life expectancy.

This inclusion of life insurance in the portfolio shifts the efficient frontier up and to the left—offering greater return with less risk. It confirms what many wealth advisors have long suspected: that life insurance is not merely a protective tool but a strategic enhancement to any efficient portfolio.

Efficient Frontier Including Life Insurance

© 2020 Lion Street, Inc. Used with permission.

Real-World Planning Implications for HNW Clients

For advisors and their HNW clients, these findings suggest a clear set of actions:

- Rethink the Role of Life Insurance: It’s no longer just about protection. Life insurance should be considered as a core component of an asset allocation strategy.

- Leverage Cash Value Strategically: Use policy surrenders and/or loans to hedge sequence-of-return risk and provide liquidity during downturns.

- Prioritize Long-Term Efficiency: While term insurance may require less outlay, it does not contribute as much to portfolio performance or offer as great of planning flexibility.Preview Website

- Consider ILIT Ownership: For estate tax mitigation and asset protection, housing the insurance in an irrevocable trust structure enhances utility.

- Model Life Insurance with the Same Rigor as Other Assets: Use actuarial return and risk projections to evaluate permanent life insurance alongside stocks, bonds, and alternative investments.

- Use Portfolio Optimization Techniques: Calculate Sharpe Ratios, expected returns, and standard deviation of the death benefit to validate the role of insurance in a diversified portfolio.

The Bottom Line: Durable Value in Uncertain Times

The integration of permanent life insurance into a comprehensive financial plan provides a unique combination of stability, tax efficiency, and legacy maximization. The EY white paper quantifies what top advisors have known for decades: in uncertain economic times, life insurance isn’t just nice to have - it’s essential.

And as the Trusts & Estates analysis shows, when properly structured and funded, permanent life insurance not only stands up against traditional asset classes but outperforms many on a risk-adjusted basis. With a low standard deviation, a guaranteed death benefit, and favorable tax treatment, permanent life insurance becomes the uncorrelated anchor that can enhance long-term outcomes in an otherwise turbulent world.

In an age of complexity, permanent life insurance offers clarity. In an age of volatility, it offers ballast. And in an age where legacy matters more than ever, it delivers outcomes that other assets simply can’t.

For HNW clients seeking to optimize both lifetime income and generational wealth transfer, it is time to think differently about life insurance. At Cedar Point Financial Services LLC, we work with clients’ legal, accounting, and other advisory professionals in developing and implementing strategies that optimize their individual and business financial plans.

Sources: EY "NextWave Insurance: Life Insurance and Retirement," Trusts & Estates: "Life Insurance as a Contingent Asset Class" by Jay C. Judas and Michael Fontanini.